Debt relief options - debt settlement and bankruptcy

Let's jump right in from last week's blog. Debt settlement enables a debtor to pay off a portion of their outstanding debt, allowing the creditor to receive something versus nothing. A debt settlement company will use their relationship to negotiate the terms of the settlement. In return for their efforts, the company receives a percentage of the original, not settled, balance of debts. According to Debt.org, the average client reduced total debt of approximately $30k - $35k. If a debtor is using this method, they are in a good bit of debt. That's the only way this can be worth all the time and effort.

This may sound familiar from our discussion about debt management plans. So what are the differences? A settlement does not contemplate full payment for the debts like a management plan. The borrower agrees to a set amount of the balance with the understanding that the remaining amount cannot be collected in the future. Often times, the debtor may be encouraged to stop payment on the debts and instead send those funds to the debt settlement company to build up an escrow account in anticipation of the settlement. As you can imagine, it can take a while to build up an enticing amount to cover the settlement. The borrower's credit can continue to decrease as months pass with no payment, but once the settlement payment is made, that is the end of the relationship between the borrower and creditor. The settled debt is viewed as a negative event that impacts your credit score and remains on your credit report for 7 years.

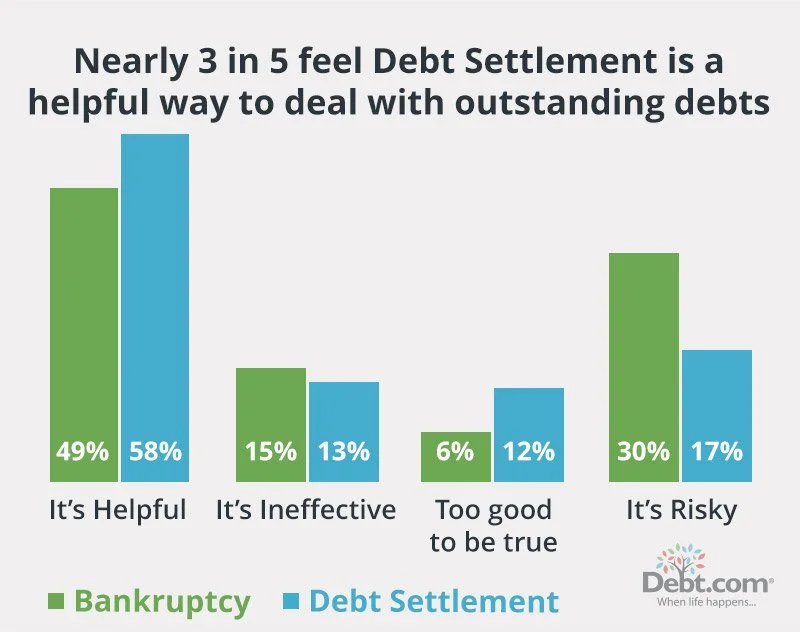

Debt settlement can also have tax implications. The IRS views the forgiven amount as 'income' to the borrower and can collect taxes for any debt settlement greater than $600. Even with those potentially negative impacts, nearly 60% of surveyed folks believe that debt settlement is a helpful way to deal with outstanding debt (Debt.com survey), compared to bankruptcy. We will get to bankruptcy momentarily.

Debt Settlement: What is it and is it right for me?, article updated April 10, 2025

What could a settlement look like for a consumer with $25,000 in unsecured debt.

Original balance - $25,000

Settled amount - $18,500

Monthly payment to debt settlement company - $390.00

Number of years - 4 years (48 months)

Fees - varied types; set up, administrative, service, maintenance - $375.00

Payment to debt settlement company - 15% of $25,000.00 = $3,750.00

Beginning credit score: 635

After credit score: 525

Potential total out of pocket for settlement: $22,845.00

If you have the time and organization to tackle settling debts yourself, here is a checklist https://www.debtconsolidationcare.com/steps.html

Again, a consumer should be well informed as they are talking with debt settlement agencies and understand the fees, payments, and terms of commitment before proceeding.

Bankruptcy

Finally, let's take a look at bankruptcy. There are two consumer options - chapter 13 and chapter 7. Chapter 13 bankruptcy is a legal remedy for wage-earning borrowers to devise a plan and intentionally repay their debts. An automatic stay is established barring creditors from attempting to collect payment from the debtors. The debtor will make monthly payment to the case trustee and those payments are distributed to the collection of unsecured creditors. Depending on the payment plan for the debtor, the bankruptcy matter can last 60 months. The bankruptcy remains on credit report for 7 years.

A Chapter 7 bankruptcy is the other legal remedy for consumers. This option involves a liquidation of available assets to pay debts. A case trustee will review all the potential debtor's income, assets and debts and assess whether the debtor is insolvent and therefore unable to repay the debts on an ongoing basis like the Chapter 13 remedy. If the debtor is determined to be incapable of repaying debts in full, the trustee will liquidate the non-exempt assets and pay creditors a percentage of what is owed. Same as a Chapter 13 case, an automatic stay is enacted to stop creditors from directly contacting the debtor to collect payment. After the Chapter 7 bankruptcy case concludes, the court sends creditors the notice of discharge closing the case and ordering creditors to stop any future efforts to collect. A chapter 7 bankruptcy negatively impacts the credit score and remains on credit report for 10 years. If a debtor completes the Chapter 7 bankruptcy process to discharge, they are barred from refiling a chapter 7 bankruptcy for 7 years.

Pursing bankruptcy should not be taken lightly, nor should it be the initial remedy for consumer debt. The cost, time commitment and damage to the credit report is a lot to overcome quickly. However, if bankruptcy is the best option, review available resources to be as educated about the process as possible. Don't be afraid to enlist the help of legal counsel. They are your advocate throughout the course of the case and help smooth out the legal process.

Let's talk about these options specific to your financial situation. Hope is not lost! There is a way out of this, but information will be your best friend. What can you do today - 100% vital - to begin moving out of this season? Hit us up on social media @StudioMFin, or email at letstalk@studiomfinancial.net. Until we meet, keep working on the change.