Credit history and utilization and score…don’t zone out!

Let’s continue our credit product discussion and review credit card history and utilization. How are these terms defined and what they can project for a consumer?

Credit history reflects how regularly a consumer uses credit products and their consistency (or inconsistency) of repayment. Lenders are more inclined to extend credit at advantageous terms when a consumer demonstrates they can repay borrowed money. Same concept in everyday life. If your 16-year-old borrows $60, and consistently repays, you are inclined to continue lending them more money in the future, right? Maybe.

Sometimes consumers want to close irregularly used credit card accounts but aren’t certain if that’s okay. Some advisors will suggest keeping them open but use them lightly and pay off the balance every month. That makes sense if the consumer has a specific purpose for the credit account. However, if the consumer keeps a credit account active without true purpose, that’s one more thing that can be overused and lead to a more challenging situation.

If the consumer desires to close accounts, they should consider the usefulness of each credit account, length of time the accounts have been opened, and future usage of credit products. Consumers should consider keeping credit accounts active that have been open for 10+ years. Lenders view consumers as responsible when they have a couple accounts with extensive history of use and repayment. Remember your teenager? The more recent the account is opened, the less lenders can determine that a consumer will be responsible with their credit product. They hope consumers will repay because of history.

If credit cards had a designated purpose, I would encourage the consumer to determine if that purpose is still necessary in their current financial situation. If not, a decision may be forthcoming. These decisions can hinge on whether a consumer anticipates using credit for a major purchase in the next 6 to 9 months. Lenders funding large purchases like a home or vehicle look very closely at credit history. This is a long-term loan on their books, and lenders want to feel reasonably confident that the borrower will repay in full and timely. Building positive credit history until the purchase is closed can work in the borrower’s favor. After the purchase has closed, the consumer can review and close whatever accounts they deem best. Just understand you are responsible for paying off the balance.

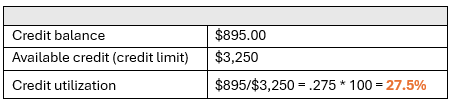

Credit history is a concept, while credit utilization is represented by a hard percentage. If you hear anyone say, “my credit utilization is 45%,” do you know what they are referring to? Most people don’t, so you aren’t alone. But let’s put you in the minority of those in the know. Credit utilization is the percentage of available credit currently in use. Available credit is the same as the credit limit. Let’s use Samantha as an example.

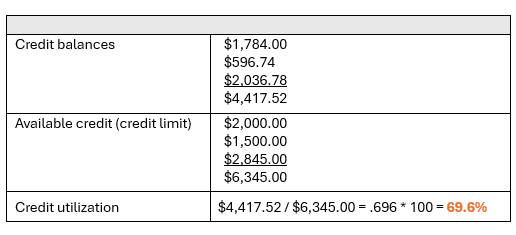

Samantha has only one card, meaning she is currently using 27.5% of credit available to her. But what if Samantha has multiple credit cards? The calculation is the same. As demonstrated below, Samantha uses approximately 70% of the credit available to her.

Quick note. The credit utilization calculation applies to revolving credit - products with a credit limit and fluctuating balance. Those include credit cards, personal lines of credit, and home equity lines of credit (HELOCs). Student loans, car loans, and mortgages do not factor in this calculation. They are folded into the debt-to-income ratio.

Using the division symbol is super rad, but what can the percentage tell us? Credit utilization can be an indicator of reliance on credit, a measure of overspending, evidence of prior financial challenges (exp., loss of job or major medical event), or low awareness of monthly expenses. A higher percentage, particularly over 50%, can be a caution flag to lenders and impact your current credit score and future terms. A high credit utilization costs consumers money now and in the future. First, if credit card balances aren’t paid in full every month, the APR will be applied, increasing the balance and raising subsequent month’s minimum payment. Second, any future credit product a consumer applies for can carry a higher interest rate, increasing the cost of using that credit product. Understanding this simple math problem can potentially save a consumer thousands of dollars.

What should you consider?

Understand the purpose for those credit cards. Why and for what are you using those credit products? Travel, household expenses, or jus’ cuz? Consider paying off and closing newer accounts. Keep your monthly obligations manageable.

Assess the current credit utilization. Stack all the credit card statements, grab a calculator and crunch the numbers. Review the calculation above as a guide.

Formulate a plan to reduce credit card balances. If the percentage is 65%, set a goal to reduce that to 50%. Or if the utilization is 50% - 65%, work to reduce that to 40%. Sweet spot is around 30%. Do this incrementally. Do not put yourself at a greater disadvantage attempting to do too quickly.

Stay away from shame. Keep to the numbers, sans emotion. The utilization could be 110%. Refuse to make a value assessment on you as a person. Stick to the facts and change the facts. You are worth it!

I’m gonna throw a changeup. I challenge you to run the utilization calculation. That’s the 100% vital. Know the numbers then decide what you want to do. StudioM Financial has calculators ready help as well. Reach out at letstalk@studiomfinancial.net or (469) 615-0387. Until we meet, keep working on the change.