Net worth statement - what does that tell me?

At what point should an individual know their net worth, and what does it tell them? My answer is: whatever point and it tells them how they are managing any accumulated debts with available assets, and what’s left over. A net worth statement can be a great decision-making tool for a household.

Let’s start here: What is a net worth statement? A net worth statement categorizes and lists all current and long-term assets against current and long-terms debts, then calculates the difference. Quick review of a few definitions so we are all working with the same information.

Current assets are those that are the most liquid (cash or can be easily converted to cash).

Long-term assets are less liquid but have the capacity to gain value for the individual every year.

Current debts are owed by an individual within the next 12 months. Current debts have a mixture of revolving and installment debts.

Long-term debts are owed by an individual for longer than 12 months. Most long-term debts are repaid by installment payments.

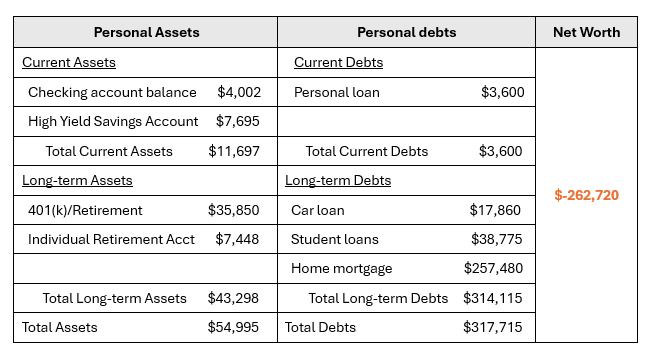

I want to give an example of how a net worth statement could be used for a household. Let’s meet Nina. Below is Nina’s first net worth statement. I will follow up with some observations, then a list of Nina’s observations and corresponding decisions. Would love to hear your observations! Throw them in the chat.

Initial observations from the first statement:

Current Assets: Nina is just getting started with setting money aside and managing her monthly budget, so the balances are modest. The balance of Nina’s high-yield account is growing due to regular contributions.

Long-term Assets: Nina is contributing close to the maximum annual limit on a pre-tax basis from her paycheck ($23,500). Similarly, she is contributing the maximum amount to her individual retirement account ($7,000). Close to $55k in total assets is a healthy start.

Current Debts: Nina has a relatively low car loan and is paying off a personal loan for a family member. Nina was the co-signer on the personal loan. The primary borrower quit paying the monthly payments, Nina to make the payments to keep the account out of default.

Long-term Debts: Nina purchased her starter home approximately 2 years ago. She graduated from college with a bachelor's degree that she is using in her current job. Repayment started on her student loans and she is in the standard repayment plan.

Nina has a large negative net worth. The bulk of that negative worth is due to her student loans and home mortgage.

Nina reviewed the initial statement and made some decisions.

Pay off the $3,600 personal loan before the original term expires.

Keep the personal loan as the only current debt until it is completely paid off. Nina has one credit card, but she pays off the balance every month to avoid incurring interest.

Nina was unfamiliar with how a certificate of deposit worked, so she opted for a short-term CD as an investing experiment with low risk. She receives dividend payments, and the initial investment will be returned to her at the end of the 9-month period. At the end of that 9 month term, she plans to roll that balance into her high yield savings account.

Nina observed that her 401(k) account is steadily growing, so she will maintain the annual contributions and adjust her monthly budget to accommodate annual 1% increases.

Nina was initially concerned about the significant negative net worth but realized that she can take a long-term view of her finances. She understands that she can increase her assets as her income increases and her investments gain value.

Nina understands that the standard repayment plan for her student loans is the highest repayment plan, but she wants to pay them off as quickly as possible.

For right now, Nina will hold off on paying extra on her house payment. She is aggressively paying down the personal and student loans and increasing other assets. The mortgage can ride for another 3 – 5 years at the current payment.

Combining those observations and Nina’s decisions, what could her net worth statement look like in 5 years.

Nina still has a negative net worth, but in 5 years she has:

Increased her total assets by almost 4x

Decreased her total debts by more than $32k

Improved her net worth nearly $200k

The main concern isn’t the amount of the net worth – positive or negative. The main concern is what decisions can be made based on that snapshot? How can we increase assets and manage the debts? Nina chose to focus her attentions on keeping her retirement and savings on track. She adjusted her monthly budget to accommodate those goals. Throughout those 5 years, she used lump sum bonus payments to put towards savings and her student loans.

The statement is also not something you should take personally. It doesn’t mean that you are good or bad with money. It gives you a snapshot view of where your money is settling. Is it settling as an asset or a debt. We can’t control all the variables, but what does your net worth statement look like now and how would you like it to look in 5 years? Those are goals in the making!!

Again, let me know your thoughts about this example. Hope to hear from you soon.

50/70/100 principle. What do you want to tackle? StudioM Financial is here to help. Reach out at letstalk@studiomfinancial.net or (469) 615-0387. Until we meet, keep working on the change.